How to Improve Your New Zealand Credit Score in 6 Months or Less

Table of Contents

If you’re like many Kiwis, your New Zealand credit score probably isn’t front of mind. After all, it’s just a number sitting somewhere in the background, right?

Wrong. Your credit score influences your chances if you apply for credit, buy now pay later schemes, mortgages, loans, and in some cases, even job opportunities.

For newcomers to New Zealand, the challenge is even tougher. Starting with no credit history feels like being invisible to the financial system, you need credit to build a credit history, but you can’t get credit without a history. It’s a frustrating catch-22 that many immigrants know all too well.

Here’s the encouraging news: with the right strategies, you can see significant improvement in your credit score within just six months. Whether you’re building from scratch or repairing past mistakes, this guide will walk you through proven methods to boost your creditworthiness quickly and effectively.

So, whether you’re planning to apply for a mortgage and need a bridging loan, or a car loan, a loan for renovations, or business finance, keep reading to learn how you can improve your credit score in six months or less.

Terminologies You’ll See on Your Credit File

Credit terminology can be confusing, but it doesn’t have to be. Once you understand these key terms, you’ll navigate credit conversations like a pro.

- Credit History: A comprehensive record of all your loan transactions, including payments, missed payments, defaults, and any credit agreements like mortgages or hire purchases.

- Credit Reports/Credit Records: A summary document that condenses your credit history into a format lenders can quickly review, sometimes including your credit score.

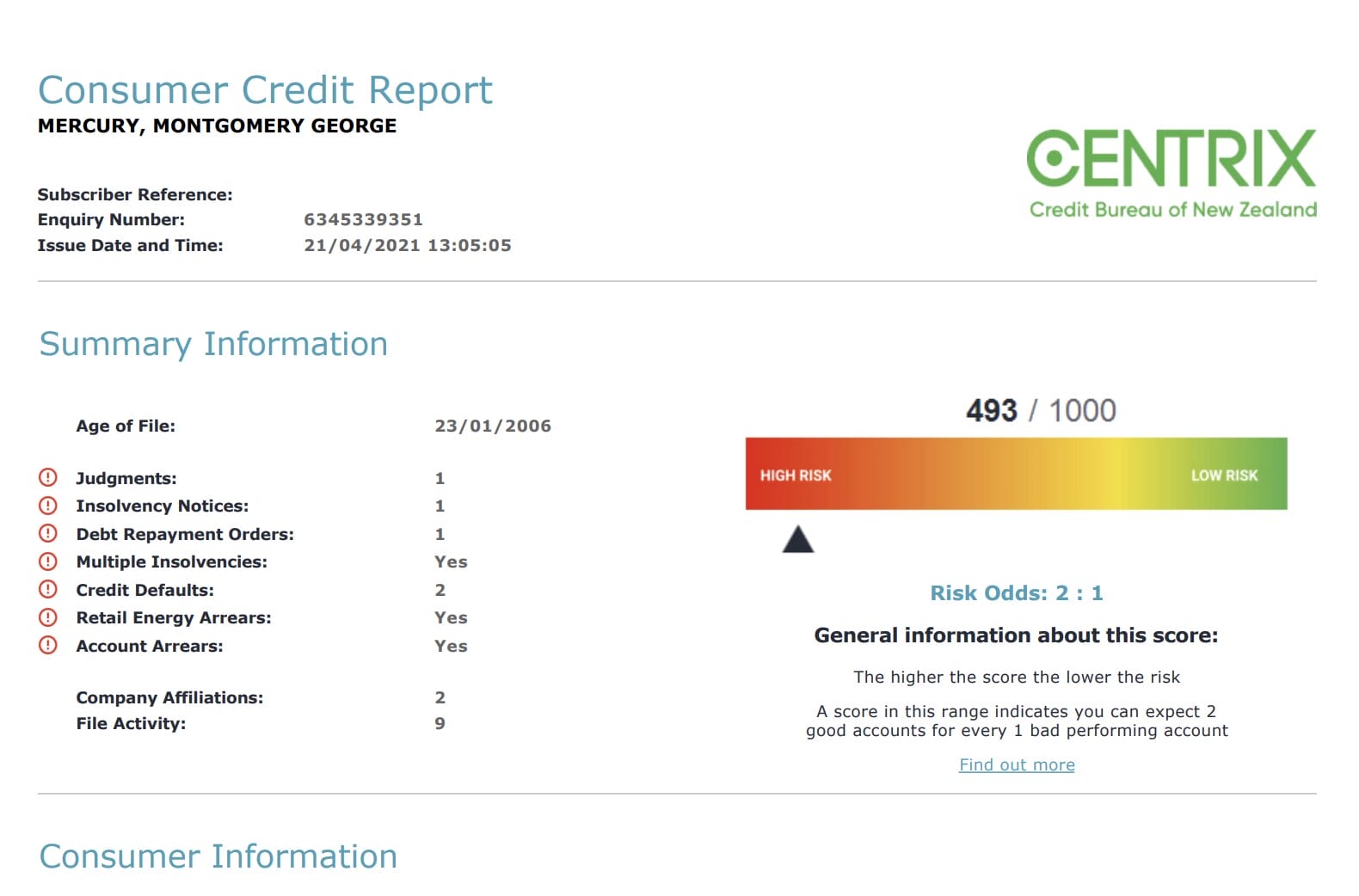

- Credit Score: A number (typically out of 1,000) that represents your creditworthiness based on your financial history. In New Zealand, a score above 700 is considered good. A credit score isn’t universal, as each agency uses a different formula.

- Credit Check: When a lender or organization requests to review your credit history to assess your reliability before approving credit applications.

How to Check Your Credit Report

You can’t improve what you don’t know. Here’s how to get a clear picture of your current credit situation.

Visit the website of one of New Zealand’s credit reporting agencies, such as Centrix, to request your report. You can get a free report per year, so there’s no excuse not to check. You can also request a fast-track credit report if you’re in a hurry because you’re applying for a loan or some major purchase. The three credit reporting agencies also have a wide range of credit report services you can avail.

New Zealand credit scores range from 0 to 1,000, with higher numbers indicating lower risk to lenders. The average credit score nationwide is 649, so anything above this benchmark puts you in good territory.

Review every section of your credit report carefully, checking that all information matches your actual credit history. Look for incorrect personal details, accounts you didn’t open, or payments marked as late when you paid on time.

According to the Sorted website, “The key to good credit is to have a clear credit history with no defaults or missed payments. If you do have a poor credit history, it’s important to take steps to improve it as soon as possible.” This sentiment is echoed by many financial experts, including Auckland-based financial advisor Sarah Verrall, who advises her clients to “keep a close eye on their credit report and take action to correct any errors or discrepancies as soon as possible.”

How Your Credit Score is Calculated

Think of your credit score as a recipe where each ingredient affects the final taste.

- Payment History. Your track record of paying bills on time carries the heaviest weight in the calculation. Late payments, defaults, and missed payments can significantly damage your score, while consistent on-time payments boost it.

- Credit Accounts. This factor looks at two things: the types of credit accounts you hold (mortgages, credit cards, personal loans) and how much you owe on each. Lenders want to see you can manage different types of credit responsibly without maxing out your limits.

- Length of Credit History. The longer you’ve been successfully managing credit and paying regular bills, the better your score becomes. This is why closing your oldest credit card can sometimes hurt your score.

- Recent Credit Inquiries. Multiple credit applications in a short period send red flags to lenders. Each inquiry can temporarily lower your score, as it suggests you might be desperately seeking credit or taking on too much debt at once.

Common Misconceptions About Credit Scores

Credit scores are surrounded by more myths than a folk tale. These misconceptions can prevent you from taking positive action or, worse, lead you to make decisions that actually damage your score.

- Checking Your Own Score Damages It. This widespread fear stops many people from monitoring their credit health. The truth? Checking your own credit score is classified as a “soft inquiry” and has zero impact on your rating. You can check as often as you like without worry.

- Your Income Determines Your Score. Many people assume a higher salary automatically means a better credit score. Your income doesn’t appear on your credit report at all. While lenders consider income during loan applications, your credit score is purely about how you’ve managed debt in the past, not how much you earn.

- You Only Have One Credit Score. Different credit reporting agencies use slightly different data and calculation methods, which means you might have multiple scores. Don’t panic if you see variations between agencies, this is completely normal and expected in the credit reporting world.

8 Strategies to Build Credit

1. Pay Your Bills on Time

Now let’s be real – debt is a heavy burden to bear. But in New Zealand, reducing your debt is kind of important. In facts, it’s finance 101 if improving your credit score.

One simple strategy for reducing debt is to pay more than the minimum credit card payments each month. It may not seem like much, but those extra payments can add up saving you stacks on interest, and of course, you’ll get a big green tick for paying off any loans ahead of time.

Another option that’s an addition to our last point is to get a loan to consolidate your debt with a lower interest rate. This bundles your debts into one simple, easy to manage repayment, and can even help you avoid paying a higher interest. This means you’ll avoid penalties and interest charges if you’re missing payments.

Here’s a quick list to get you on track:

- Pay more than the minimum payment each month. This can help you pay down your debt faster and save money on interest.

- Consider consolidating your debt into a single loan with a lower interest rate.

- Create a budget and stick to it. This can help you identify areas where you can cut back on spending and put more money towards paying down your debt.

- Avoid taking on new debt while you’re trying to pay off your current debt. This can make it harder to make progress and improve your credit score.

- Don’t be afraid to ask for help if you’re feeling overwhelmed by debt. There are plenty of support services available in New Zealand that can help you manage your debt and get back on track.

A Word on Defaults

Defaults are the credit score equivalent of a permanent marker stain, they stick around even after you’ve cleaned up the mess.A default occurs when a payment over $125 is overdue by more than 30 days and your lender has attempted to recover the money. Even if you pay the full amount later, this black mark remains on your record with the credit agencies.

The Five-Year Shadow that will Affect Your Credit Profile

Defaults can impact your credit score for up to five years. The good news is the negative impact gradually diminishes, as you demonstrate improved payment behavior.

Here are two resources that can be of assistance:

- Sorted.org.nz: This is a free online platform that provides financial resources and tools to help Kiwis get sorted with their money. They offer a variety of tools and calculators to help with budgeting, debt management, and retirement planning.

- MoneyTalks: This is a free helpline service provided by the New Zealand government that offers confidential financial advice and support to individuals and families in need. They can help with debt management, budgeting, and financial planning.

2. Improve Your Credit Rating by Reducing Your Debt

If you’re struggling with debt, negotiating with lenders can help you lower interest rates or create a payment plan. Contact your lenders and explain your situation. Many creditors are willing to work with you to find a solution that works for both parties.

Remember, building good credit takes time and effort, but it’s worth it in the long run. By using credit responsibly, paying down debt, and negotiating with creditors, you can improve your credit score and secure a stronger financial future in New Zealand.

Building good credit is needed for securing loans, credit cards, and mortgages with favorable terms. To build your credit, you need to use credit responsibly and make timely payments.

Here are some tips that can help:

- Pay down high credit card balances. They have a negative impact on your credit score. Consider using a debt snowball or debt avalanche method to pay down your debts faster.

- Use credit responsibly: Only use credit for purchases you can afford to pay back, and avoid opening too many new accounts at once.

3. Check Your Debt-to-Credit Ratio

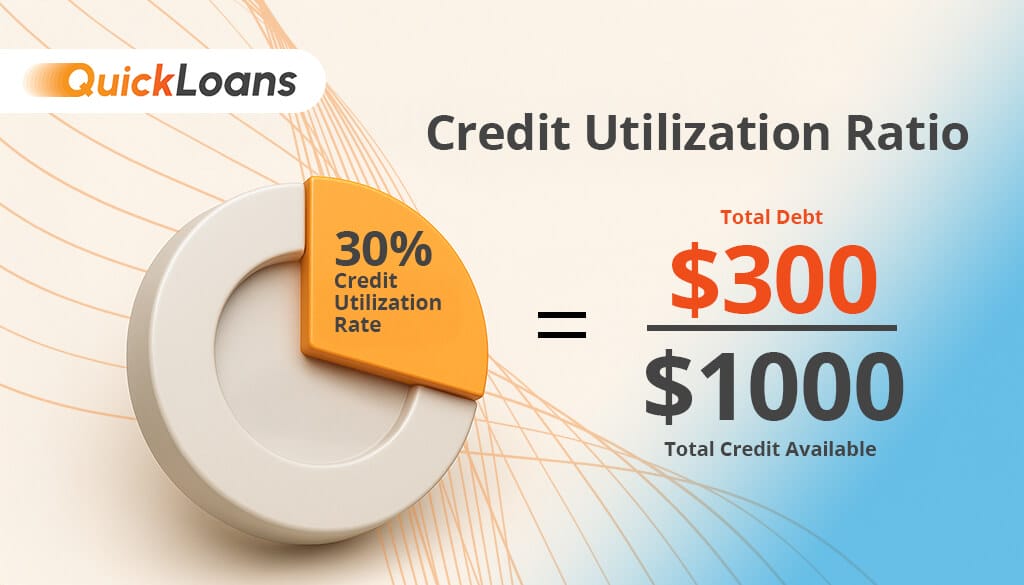

Your credit utilization ratio is like a financial fitness test. It shows lenders how well you manage available credit without maxing out your limits.

This ratio isn’t just about how much debt you’re carrying, but how much of your available credit you’re actually using. The calculation is straightforward: divide your current balance by your credit limit, then multiply by 100.

For example, if you have $300 on a credit card with a $1,000 limit, you’re using 30% of your available credit. If that same $300 was on a card with a $2,000 limit, your ratio drops to just 15%. Low credit usage show lenders that you’re not desperately relying on credit to get by.

One way to improve your ratio is requesting a higher credit limit. If you keep your spending the same but double your limit, you’ve instantly halved your utilization percentage. However, this strategy requires serious self-discipline. What’s worse, many lenders treat your entire credit limit as potential debt when assessing future loan applications. That $10,000 credit card limit might be seen as $10,000 of possible debt, reducing your borrowing capacity for mortgages or other major purchases.

The safest approach is to focus on paying down existing balances rather than increasing limits.

4. Apply for New Credit or Increase Your Credit Limit

Now this needs to be considered carefully and seems a contradiction to what we’ve written previously. Having a higher credit limit doesn’t mean you have to use it, and it can provide a range of benefits, from increased purchasing power to improving your credit score.

Here are some things to keep in mind if you’re considering requesting a credit limit increase:

Benefits of a higher credit limit:

A higher credit limit can give you more flexibility to make large purchases or handle unexpected expenses. It helps you avoid your overdraft limit and avoid penalty fees.

How to request a credit limit increase:

Contact your bank or lender and ask if you’re eligible for a credit limit or overdraft increase. You may need to provide information about your income and employment status, and it’s always best to ask for this increase when financial times are good. Your NZ bank may request an express credit report on you to check if you’re eligible.

Considerations:

Be sure to consider your ability to manage a higher credit limit and avoid overspending. Also, keep in mind that a credit limit increase may result in a hard inquiry on your credit report, which can temporarily lower your credit score.

5. Diversify Your Credit

Think of your credit portfolio like an investment portfolio, variety can work in your favor. Demonstrating you can handle different types of credit simultaneously shows the relevant credit providers that you’re a well-rounded borrower.

What a Good Mix of Credit Card Debt and Loans Look Like

An example of diversified credit might include having a mortgage, car loan, and credit card. This combination shows you can manage long-term fixed payments (mortgage), shorter-term installments (car loan), and revolving credit (credit card) all at once.

Responsibly maintaining this mix of short- and long-term, plus fixed payment and revolving credit, could boost your credit score. However, this isn’t a suggestion to take on more debt than you actually need.

6. Be Picky When You Apply for a Credit Product

Research interest rates, fees, and rewards across different lenders before opening any new account.

Choose a credit product that genuinely matches your financial needs and goals, whether that’s a low-interest credit card for emergencies, a payday loan, a rewards card for groceries, or finding the best personal loan for your personal expenses. Not all credit product or loan offers are created equal.

If you get rejected for a loan, don’t just apply right away. The credit agencies are notified every time you apply for credit, so successive applications might get your profile flagged.

The key is strategic selection, not random accumulation of credit accounts.

7. Don’t Close Your Oldest Account

Your oldest credit account is like a fine wine, it gets more valuable with age. The length of credit history makes up 15% of your FICO® Score and is heavily influenced by the age of your oldest and newest accounts. Closing an old account can undo years of credit-building work in a single decision.

While you’ll naturally close loan accounts once they’re paid off, credit cards can remain open indefinitely, continuing to give you stronger credit as the years go by.

How Keeping Old Credit Cards Active can Affect Your Credit Score

Even if you’ve moved on to better cards, keep your oldest account breathing with occasional use. Put a small recurring bill on it or make a purchase every few months to prevent the issuer from closing it due to inactivity. You can even set up a direct debit payment to it so you don’t get charged with late fees.

If your old card charges an annual fee or no longer meets your needs, contact your existing bank about to get a credit card with a better interest rate. Most banks offers a range of credit cards, and many of them will be happy to give you a better deal based on your credit history.

8. Deal with Errors on Your Credit Report

Credit report errors are more common than you might think, but the good news is you have clear pathways to fix them. Being proactive about spotting and correcting mistakes can give your credit score an immediate boost.

How to Report Loan or Credit Card Errors on Your Credit Report

- Check Regularly. Get a comprehensive credit reporting by obtaining reports from all major credit agencies. Different agencies might have different information, so don’t rely on just one source.

- Identify Inaccuracies. Look for incorrect details about late payments, outstanding debts that aren’t yours, or identity mix-ups where someone else’s information appears on your report.

- Contact the Reporting Agency. Equifax, Centrix, and every credit agency has an established dispute processes to correct errors. Contact the credit reference agency and follow their instructions.

- Provide Supporting Documentation. Gather evidence like bank statements, proof of payments, or correspondence that supports your dispute. Solid documentation strengthens your case significantly.

If the credit reporting company refuses to make corrections you believe are justified, you can escalate to the Privacy Commissioner. They’ll investigate the issue independently. Should the matter remain unresolved, it can proceed to the Human Rights Review Tribunal for a final determination.

Got Bad Credit? It’s Not to Late to Improve it

In conclusion, there are many ways to improve your credit in New Zealand, but you can’t do it overnight. With the right strategies, tools, and mindset, it’s achievable in six months or less. Here’s a quick recap of the key strategies we covered in this New Zealand guide:

- Check your credit report regularly, and dispute any errors or fraudulent activity. You can request your free report and check your credit score for free as well once a year.

- Make sure your credit balances are low to maintain a healthy credit utilisation ratio.

- Pay down debt using the debt snowball or debt avalanche method, and negotiate with creditors for lower interest rates or payment plans.

- Consider requesting a credit limit increase, but only if it won’t tempt you to overspend.

- Don’t close old credit cards because it will hurt your credit score

- Open a new credit account strategically, considering the impact on your credit mix and payment history.

Remember, improving your credit score is a journey, not a destination. It takes patience, discipline, and a willingness to learn and adapt. But by taking action and implementing the strategies we’ve discussed, you can start seeing results and achieve your financial goals.

by Ash Horton

02/05/2023

Ash is a professional content writer with extensive experience in business development in the financial services. Ash has founded businesses from the age of 19, including franchising ventures, and working alongside some of the largest retailers in the world.