Creating a Retirement Planning Strategy that Works for You

Table of Contents

Your grandmother probably retired with a pension that covered most of her expenses. Your parents might scrape by with a mix of retirement savings and NZ Super. But what about you? With healthcare costs climbing and pensions becoming as rare as handwritten letters, the typical retirement planning advice doesn’t work anymore.

Setting retirement goals isn’t about hitting a magic number. When your plan for retirement aligns with your values, you create something more powerful than a savings target. You build wealth that lasts and decisions that stick.

This guide will show you how to start planning for retirement in New Zealand. We’ll discuss how childhood experiences shape your money decisions, discover strategies for different stages of retirement, and give you a framework for building a financial plan that excites rather than overwhelms you.

Why Your Money Mindset Matters More than You Think

The biggest barrier to successful retirement planning isn’t market volatility. It’s the beliefs you have about money. These mental patterns, formed early in life, quietly steer every investment strategy and financial decision you make.

6 Money Mindsets that Affect Everyone’s Retirement

- Money Avoidance

You associate finances with stress and ignore them completely. This leads to procrastination on opening KiwiSaver accounts or reviewing your investment portfolio. - Money Worship

You believe money solves everything and focus obsessively on earning more. You might overwork while neglecting to save and invest what you earn. - Money Vigilance

You’re extremely careful with spending but worry constantly about security. Extreme caution can prevent you from taking risks in your choice of asset class and how you save for retirement, leaving your money in a low-return savings scheme. - Money Status

You equate financial worth with personal value. This drives impulsive spending to maintain appearances while your retirement savings and long-term goals suffer. - Risk Aversion

Research from Columbia University shows people become more loss averse as they age. Older adults feel losing money 10 times more intensely than gaining the same amount. Waiting too long to invest for retirement doesn’t just cost time, it costs money too. For instance, if you invest $50,000 at age 25 and earn an average annual return of 7%, your nest egg could grow to about $748,722 by the age of 65. But if you wait until age 35 to invest that same $50,000, you’d end up with only around $380,612 by 65. The lesson? Invest early if you want to achieve the income you want in retirement.

- Affinity Traps

Taking financial advice from people just because you like them, regardless of their expertise. Your brother-in-law might excel at fantasy football, but that doesn’t qualify him to guide your grow your retirement income.

Building Your Personal Retirement Vision

Now that you understand how mindset shapes your financial decisions, it’s time to get specific about what you want from retirement. Most people skip this step and jump straight to crunching numbers, but that’s backwards thinking.

Your desired retirement lifestyle should drive your plan, not the other way around.

What Does Your Ideal Retirement Lifestyle Look Like?

Close your eyes and imagine you’re 65 years old.

What are you doing on a typical Tuesday? Are you volunteering at the local animal shelter, taking pottery classes, or video-calling grandchildren across the country? Maybe you’re traveling through Southeast Asia or finally writing that novel you’ve been thinking about for decades.

This isn’t just daydreaming. The retirement lifestyle you envision determines how much money you’ll need.

Someone planning who dreams gardening and reading will need to save far less than someone wanting to cruise the Mediterranean twice a year.

Think about these key areas:

- Housing: Will you stay in your current home, downsize, or relocate somewhere with lower cost of living? Your housing situation dramatically impacts your retirement savings.

- Activities: Do you want an active retirement lifestyle filled with travel and hobbies, or a quieter lifestyle focused on family and community? Active retirements cost more but might also keep you healthier longer.

- Family: Will you be supporting adult children or aging parents? Are you planning to leave an inheritance or spend most of your wealth during your retirement years?

- Living Expenses: How much do you spend on average in utilities, groceries, and other daily necessities? Calculate that per year and add inflation too. Even if you own your family home outright, you’ll still face property taxes, insurance, and upkeep costs. Seek professional advice to crunch these numbers.

- Healthcare: What’s your family health history? Planning for potential medical needs isn’t pessimistic, it’s practical. Health insurance premiums, prescription medications, dental and vision care, and potential long-term care can consume a huge chunk of your budget.

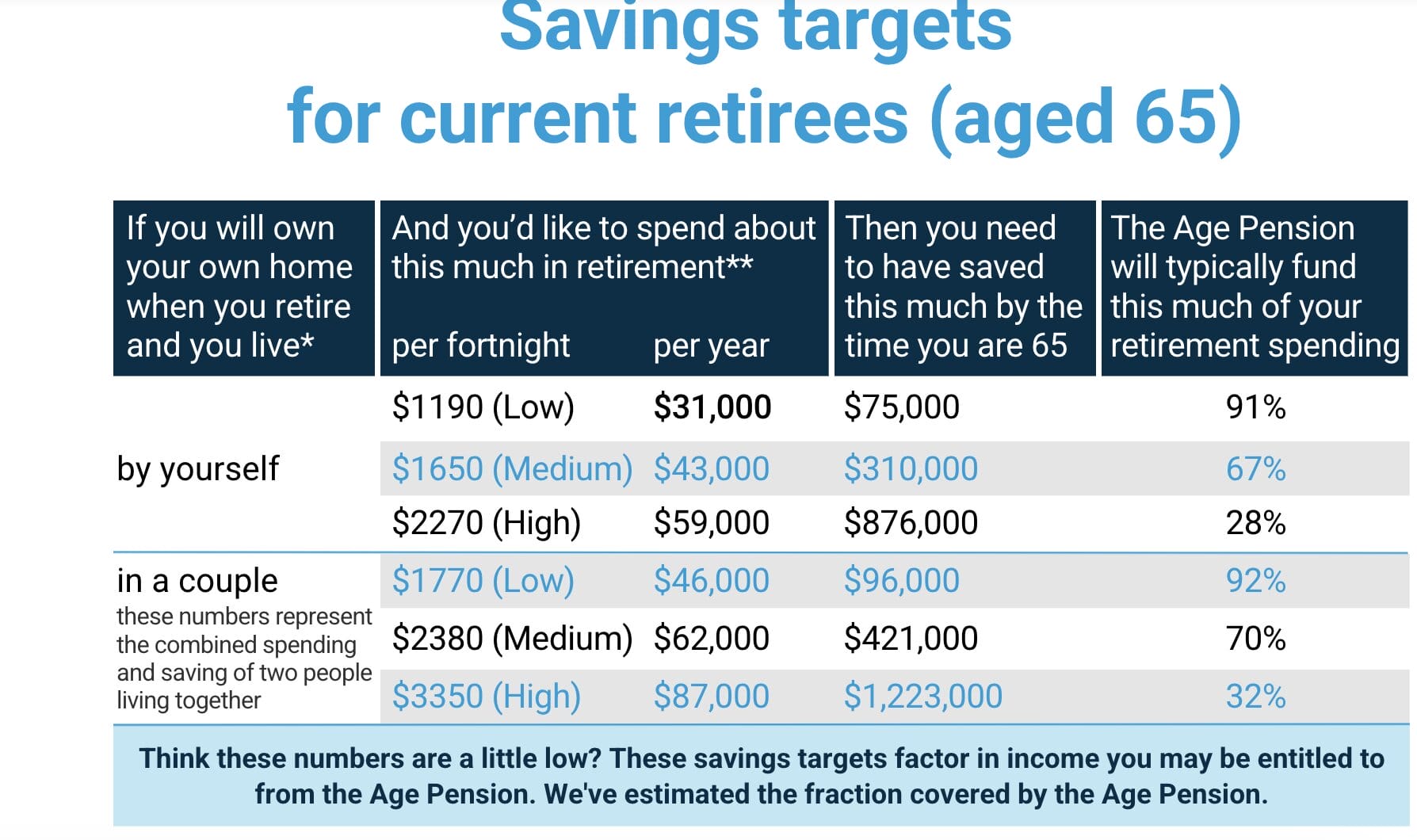

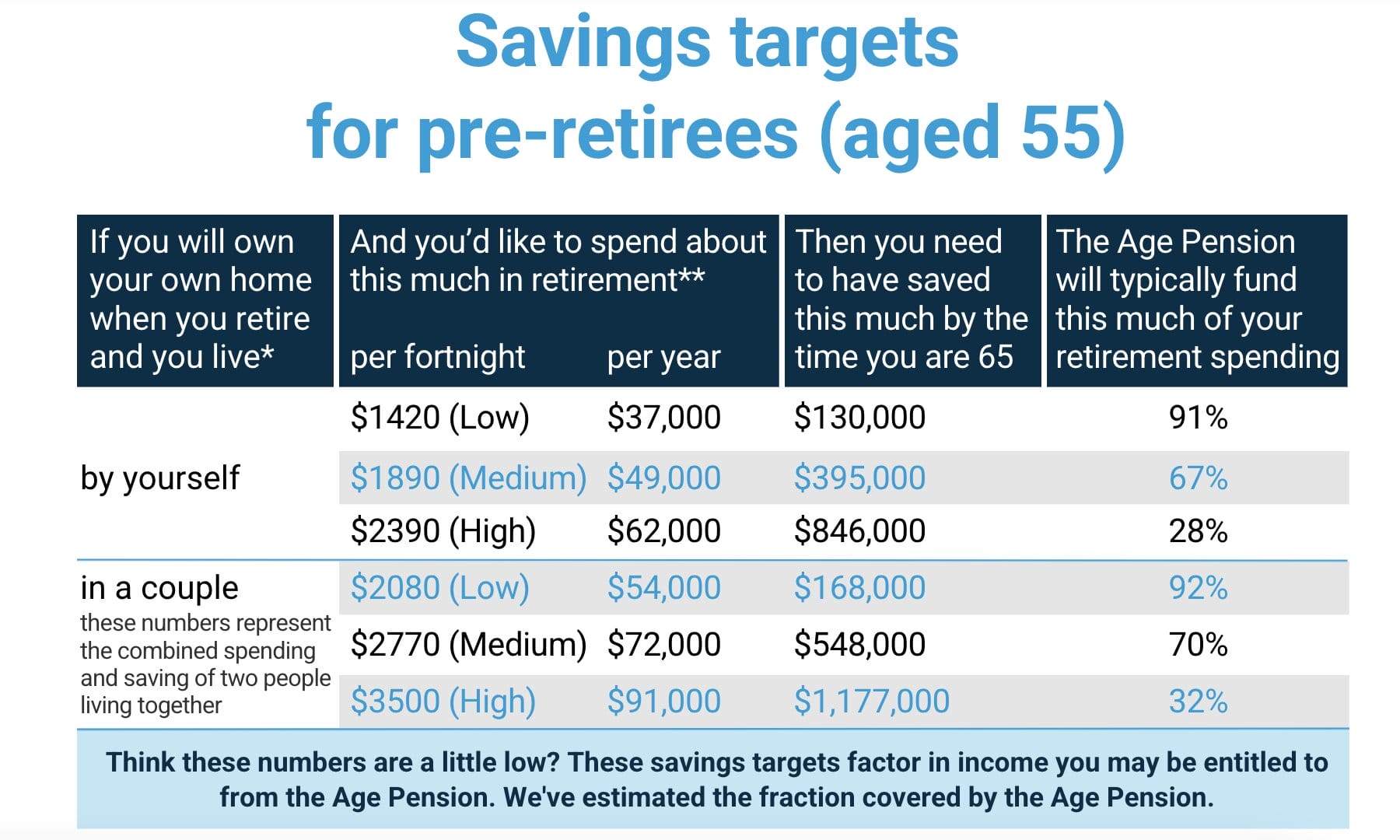

Understanding What Retirement Actually Costs

Here’s where many people get a reality check.

Recent data from the Association of Superannuation Funds of Australia shows that couples need around $70,500 annually for a comfortable retirement, while singles need about $50,000.

Of course these are just starting points. Your personal needs to live comfortably might be different.

These tables assume that you own your home and are not paying a mortgage or house renovation loan. Spending levels have also been adjusted for today’s dollar value and inflation rate as of January 2025.

Why Location Matters in Your Retirement Plan

Where you retire can make a $20,000 annual difference in your budget. Moving from an expensive city to a smaller town with good healthcare and amenities can stretch your income during retirement significantly.

Consider proximity to public transportation, which becomes more important as driving becomes challenging. Access to quality healthcare facilities is crucial. And don’t forget about social connections—moving somewhere cheaper but isolated from friends and family might save money while costing happiness.

If you’re still paying off your home, factor this into your timeline. Some people delay retirement until they pay off the mortgage, while others plan for retirement by making payments from their KiwiSaver contributions or NZ Super. Either approach can work, but you need to account for it in your financial plan.

Planning for the Three Phases of Retirement

Here’s something most people don’t realize: retirement isn’t one long, unchanging period.

It’s three distinct phases, each with different needs, priorities, and spending patterns. Understanding these stages helps you start planning more effectively and avoid nasty financial surprises down the road.

Consider this: if you retire at 55, you could spend your retirement funds for 30 years or more. That’s longer than many people’s entire careers. Your needs at 55 will be completely different from your needs at 85, so your financial plan should reflect that reality.

The Numbers Behind Your Retirement Savings

According to the Australian Bureau of Statistics, the average retirement age in New Zealand sits at 55.4 years, with women typically retiring one to three years earlier than men. With life expectancy reaching 85 for women and 81 for men, you’re looking at potentially many years of retirement to fund.

This creates what financial planners call “longevity risk,” the very real possibility that you’ll outlive your nest egg if you don’t begin planning carefully. Breaking retirement into phases will help you allocate resources better across these decades.

Early Retirement: The Active Years (Ages 55–70)

The first phase is the most expensive and active. You’re healthy, energetic, and finally have time for all those things you put off during your working years. This is prime time for travel, new hobbies, and catching up with family and friends.

Focus these early years on:

- Setting up sustainable income streams: This is when you transition from earning paychecks to drawing from your KiwiSaver scheme, NZ Super, or personal investment strategy.

- Budget adjustments: Moving from full-time income to retirement income requires recalibrating your spending. This adjustment period can be tricky, especially if you’re relying primarily on New Zealand superannuation.

- Major purchases and travel: If you’re planning big-ticket items like RV purchases or extended overseas trips, budget for these early. Your energy and health are at their peak now, so this is the time to tackle ambitious travel goals.

- Part-time work considerations: Would you stop working entirely? Many people continue to work and keep flexible hours in early retirement. This isn’t just about extra income, it provides social connections and purpose during the transition period.

- Estate planning updates: Make sure your will, powers of attorney, and beneficiary nominations reflect your current situation. Set annual reminders to review these documents.

Middle Retirement: The Settled Years (Ages 70–80)

You’ve established routines, found your rhythm, and can fully embrace the freedoms that retirement offers. Interestingly, spending often starts declining during this stage as travel becomes less appealing and lifestyle needs stabilize.

Focus areas include:

- Community engagement: This is when many retirees get deeply involved in volunteering, mentoring, or contributing to causes they care about. These activities provide purpose and social connections. Allot money for these activities.

- Personal development: Finally have time for that pottery class or language learning you’ve been postponing? This stage is perfect for exploring interests that got pushed aside during your career.

- Health maintenance: Staying physically and mentally active during these years pays enormous dividends in quality of life. Regular exercise, social engagement, and mental stimulation become increasingly important. Of course, you’ll also need to allot funds for maintenance medicines and routine medical check-ups, on top of what you’ll need for other ailments that will arise due to age.

- Social connections: Maintaining strong relationships with family and friends requires more intentional effort as you spend your retirement years. Remember to allot money for joining clubs and participating in community events. Helping your kids with their family home, renovations, or childcare also requires budgeting on your end.

Later Retirement: The Security-Focused Years (Age 80+)

The final phase shifts focus toward stability, security, and maintaining quality of life. While some people remain remarkably active into their 80s and 90s, this stage typically involves more assistance with daily activities and increased healthcare needs.

Key planning areas include:

- Financial security review: Carefully assess whether your income streams and remaining KiwiSaver savings can sustain you. Understanding government support options like the government pension or Work and Income assistance becomes more critical as other resources potentially dwindle.

- Healthcare and support planning: Explore aged care options and in-home assistance services before you need them. Understanding costs and available services makes transitions smoother and less stressful for everyone involved. If all else fails, we also offer emergency or medical loans.

- Legacy considerations: Think deliberately about what you want to leave behind, whether financial support for family, charitable contributions, or personal stories and memories for future generations.

Your Retirement Roadmap Starts Here

Setting retirement goals isn’t about finding one perfect number. It’s about understanding your values, recognizing your money mindset, and planning for retirement in phases. Once you’ve clarified what you want from retirement and how your needs will evolve over time, you’re ready for the next crucial step: using a retirement calculator to figure out exactly how much you’ll need to retire.

Stay tuned for our follow-up guide on crunching the numbers and creating your personalized retirement savings strategy.

31/08/2025

Charley helps finance and B2B companies in the AU/NZ market to increase sign-ups through conversion-focused content marketing and email campaigns. She writes about insurance, lending, real estate, and all things money. Loves cooking and gardening.